The below article is written by Kieran Maguire, a Senior Teacher in Accountancy in our Management School. He co-hosts The Price of Football podcast.

The pantomime for adults that is the 2023/24 football season has started, and the biggest show in town, the Premier League, is about to join the party, and from a financial point of view it is bigger, if not necessarily better, than ever.

Following lockdown and with a cost-of-living challenge for many consumers there were concerns that fans might be cautious about spending money on the game, but this has not been born out in practice.

Income

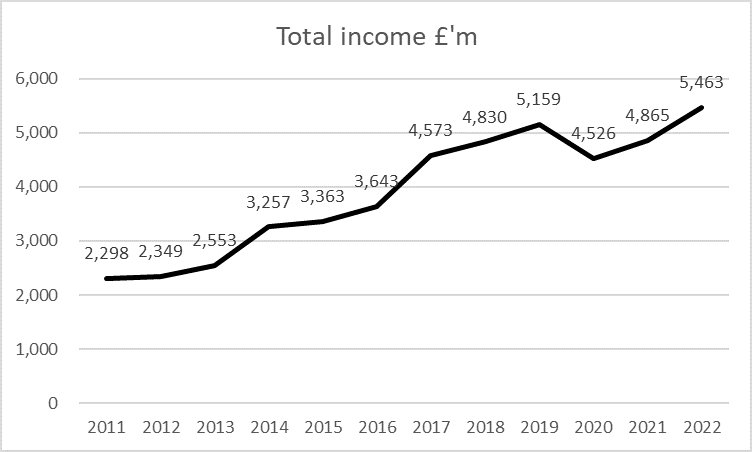

Nearly all clubs have published their accounts for 2022 and they reveal record income in the Premier League. When the competition started in 1992/93 the then 22 clubs generated £205 million between them. Fast forwards to 2022 and income has increased by 2,561%, in a period when the consumer price index has increased by 94%. All three main drivers of football club income, ticket sales, commercial activities, and most of all broadcast revenues, have far outstripped general price movements.

For the forthcoming season fans will have already noticed that they are being expected to dig deeper to fund their football habit. Season ticket prices have increased as almost all clubs, with the likes of Fulham and Aston Villa forcing through double digit rises. Clubs are aware of waiting lists for season tickets and are prepared to deal with supporter discontent safe in the knowledge that grounds will be at capacity as they have been for many years.

The only major club to freeze prices have been Chelsea, who finished 12th last season under the new ownership team, who appeared to lack familiarity with many aspects of running a football club and this was reflected in a bottom half finish, despite spending a record amount on transfers.

Merchandise prices have increased in price too, with some clubs now charging £80 for a shirt, and well over £100 for the ‘match authentic’ version. With the rise of football tourism and celebrity endorsements the athleisure market is very buoyant and there is little indication of demand falling despite the price rises.

In terms of broadcasting rights, international revenues now exceed the Premier League domestic figures. Whilst there has been a plateau in the amounts paid by the likes of Sky, BT Sport, and Amazon for domestic rights in the last two sets of rights sold, expect negotiations the next round to show an uplift as more matches are screened live.

The gap between the ‘Big Six’ clubs, about to be joined by Newcastle following the club’s acquisition by the Saudi Arabian Public Investment Fund and the remainder of the Premier League clubs continues to grow, reflecting a broader socio-economic issue of wealth inequality increasing. The ‘Big Six’ now generate on average £345 million more than the smaller clubs such as Crystal Palace.

There have been explicit attempts to increase these gaps further by the likes of Project Big Picture and the European SuperLeague, where the apologists and cheerleaders for such ideas try to market the idea of the rich becoming richer is good for the game. With their plans thwarted by vocal opposition, including most of the legacy fans of the clubs who stand to benefit, expect to see more subtle attempts to widen the difference between the elite and the also rans.

Costs and Profits

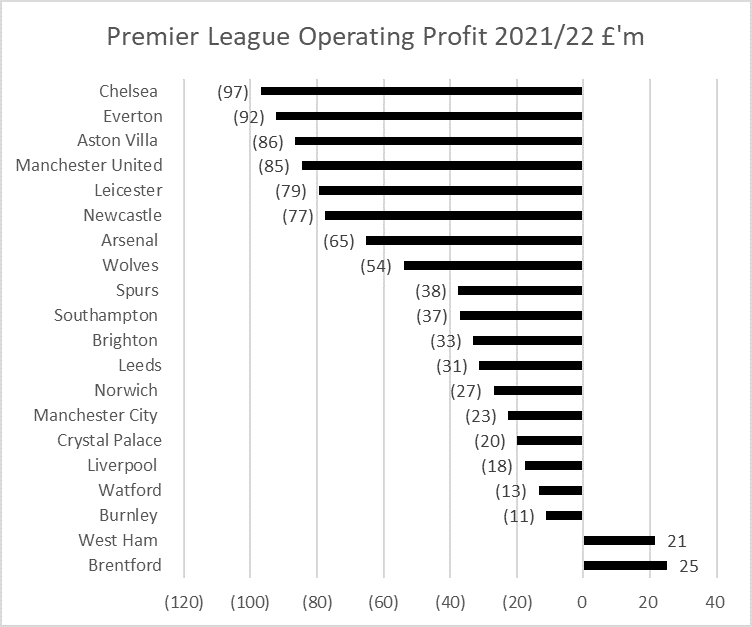

The increase in revenues should therefore be good news for clubs, yet only two clubs made an operating profit in 2021/22. Of these two clubs, Brentford were newly promoted to the Premier League and thus had by the standards of their peer group a very low wage bill, and West Ham have the benefit of operating from a stadium that is heavily subsidised by the taxpayer.

The reason why clubs are losing money is down to poor cost control. Wages in 2022 were 16% higher than in 2019, the last season not impacted by Covid, compared to income increasing by 6%. The reason for this is that clubs are highly incentivised to overspend.

At the top of the table the rewards for Champions League qualification are significant, with the winners last season, Manchester City, earning about £110 million in prize money alone. At the bottom of the table, the price of relegation for the likes of Leeds and Leicester could also reach £100 million compared to their 2022 revenues.

To reduce these losses clubs have either had to sell players or rely on funding, sometimes from financial institutions but more often from owners. Total borrowings are now £4 billion, and that is despite former Chelsea owner Roman Abramovich writing off about £1.5 billion in loans from one of his offshore companies in the British Virgin Isles.

Transfers

The summer of 2023 has been notable for an obsession with the football player transfer market, with traditional and social media speculation and neurosis at all time high levels. Those fans whose self worth is measured vicariously through their football clubs see spending someone else’s money as a vindication of their commitment. Therefore, every rumour of a recruit to the club is pored over and dissected, with the firm belief that change is the same as improvement.

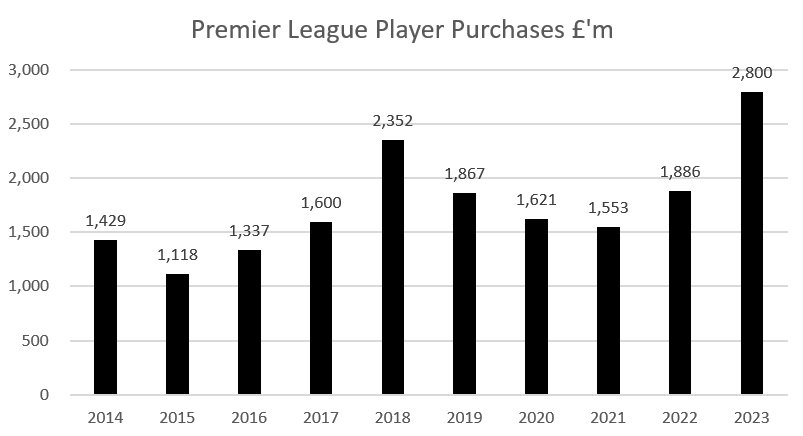

The ‘easy fix’ solution that is now the common perception of the transfer market have therefore given rise to increased prices being paid and records broken. The total spent is over £400 million more than the previous record. Consequently, many clubs are now making their player acquisitions and paying via instalments, and the Premier League’s collective credit card bill was almost £2 billion at the end of the 2021/22 season, and almost certain to rise sharply.

Despite the record amount of money being spent, only one team can win the Premier League, only four can qualify for the Champions League and three will still be relegated. There will be drama, tears, and high tension, and that’s when I find out how much the team I support has increased the price for a large bag of Starburst this season. Overall we can expect the football to be even more exciting, or at least so we will be told!