Costas Milas is Professor of Finance in the University of Liverpool’s Management School

The opening remarks of Bank of England Governor, Mark Carney at the Bank of England conference on ‘Independence – 20 years on’ flagged the importance of moving to an inflation targeting regime in 1992.

In fact, ‘inflation target’ was mentioned as many as five times during his speech. Mark Carney noted how much more volatile and higher (UK) inflation was during the 1970s and 1980s, that is, prior to the introduction of inflation targeting.

The United Kingdom adopted inflation targeting in October 1992 after exiting the European Exchange Rate Mechanism. Initially, a target range of 1% – 4% was set based on the Retail Price Index (excluding mortgage interest rate payments) measure and the target was switched to 2.5% when the Bank of England was given operational independence in May 1997. In December 2003, a new inflation target of 2% was set based on the Consumer Price Index (CPI) measure. When the Bank of England was granted operational independence in May 1997, the decision on interest rates was delegated by the Chancellor of the Exchequer to the Bank’s Monetary Policy Committee (MPC).

Over the last 20 years or so, inflation targeting has become an important tool for monetary policy. It has been suggested that the significant reduction both in the level of inflation as well as inflation variability observed is related to inflation targeting.

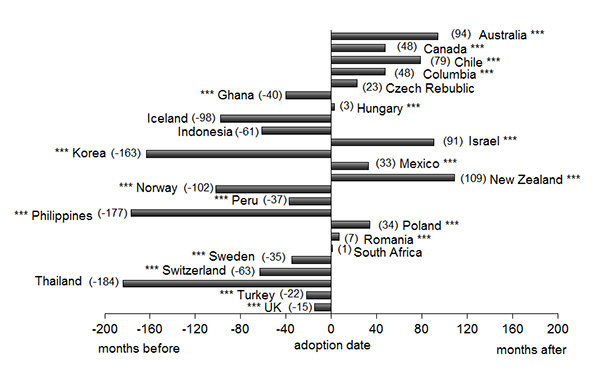

On-going research of mine (joint with Dr Theologos Dergiades from the University of Macedonia in Greece and Dr Theodore Panagiotidis from the University of Macedonia in Greece) which will appear shortly as a Central Bank of Estonia Working Paper (entitled “An assessment of the Inflation Targeting Experience”) provides an assessment of the inflation targeting experience. By focussing on 45 developing and developed countries (some 25 inflation-targeters), our work relies on econometric techniques to assess whether the adoption of inflation targeting has made a significant difference to the persistence and variability of inflation.

Our results are summarised as follows.

- For the inflation-targeters, there is a statistical difference between the formal adoption date of inflation targeting and the estimated date which the model judges as important for finding a change in the characteristics of inflation. These differences (in months) are recorded in Figure 1. In the UK, for example, we found that UK inflation changed characteristics some 15 months prior to the formal adoption of inflation targeting.

- Inflation-targeters have not necessarily been more succesful than non-inflation targeters in making inflation less persistence and/or reducing the variability of inflation.

- What matters instead for successfully taming inflation is the quality of the institutional framework within which Central Banks operate. This is definitely true for the UK. Official data compiled by the World Bank for as many as 215 countries show that the UK is ranked in the top 7% in terms of government effectiveness (which captures the quality of public services, the quality of the civil service and the degree of its independence from political pressures) and in the top 5% in terms of ‘regulatory quality’ (which captures the ability of the government to formulate and implement sound policies and regulations that promote private sector development).

- Our results do not argue against inflation targeting policies. Rather, we view the quality of central banks and institutions as a vital element in ensuring economic and financial stability in the aftermath of the recent financial crisis and the current attempt by Central Banks to gradually raise near-zero policy rates in order to return to economic ‘normality’.